The question, asked in the bankruptcy context, is whether the reorganized debtors can afford to replace their current “self-bonds” (in which the company pays for the reclamation of the site) with reclamation bonds backed by third parties.

Focusing on Peabody, this paper argues that the company's financial projections suggest it could. Therefore, for policy reasons, regulators should require it.

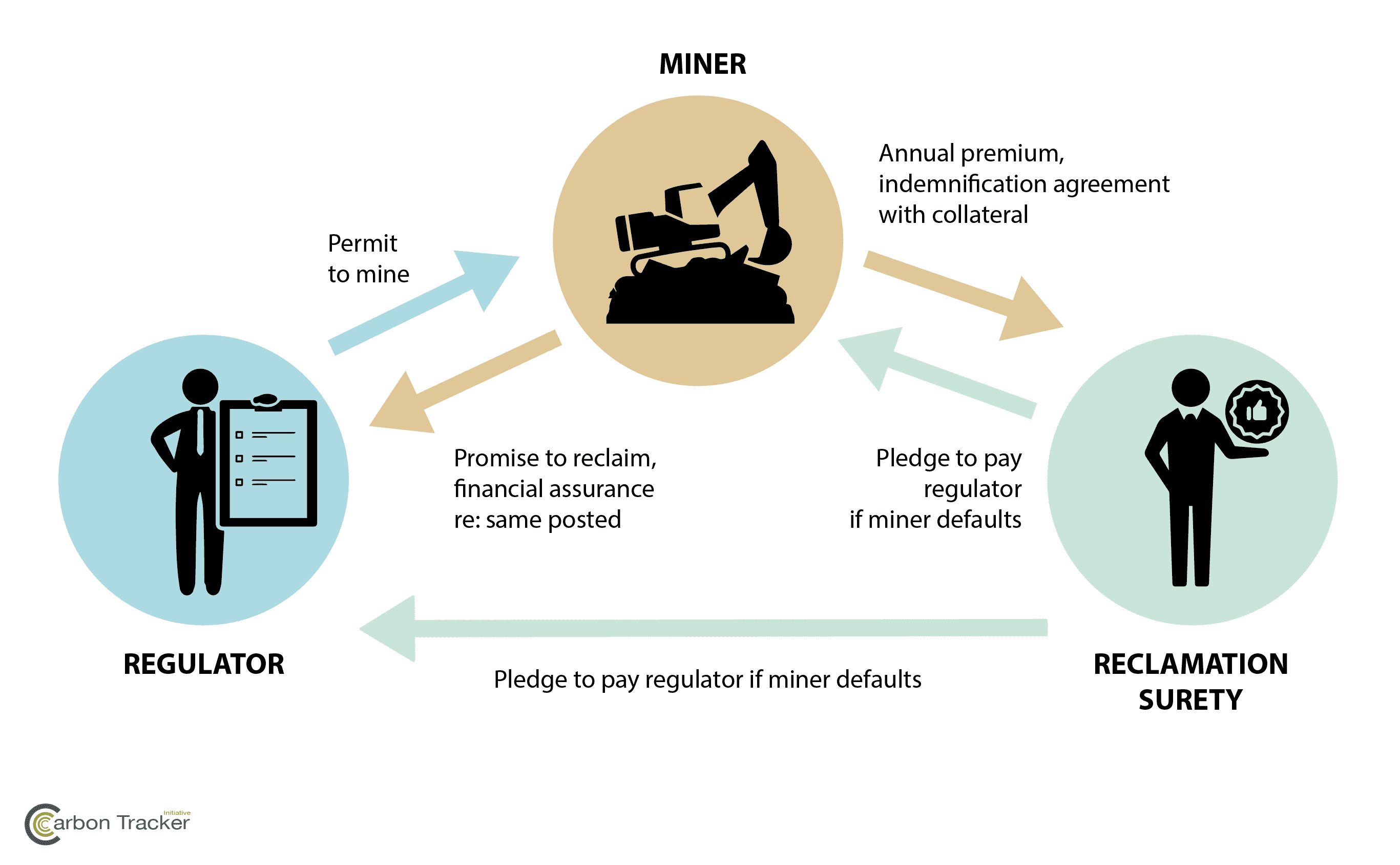

[caption id="attachment_4884" align="aligncenter" width="600"]

Structure of the reclamation bond.[/caption]